How to develop Digital payments? or maybe how to reduce the use of Cash?

- Nadim Samna

- Apr 2, 2018

- 10 min read

Updated: Aug 26, 2019

One of the most striking differences between banking in Europe and in Egypt is cash management. Withdrawals and deposits of cash are the dominant operations in the Egyptian banking branches. It is frequent to meet customers with big bags of money in or out of banking branches. In Europe, anti-money laundering laws and electronic payments popularity made large cash operations extremely rare. The diffusion of online banking tools and features made banking branches empty except maybe on Saturday mornings even after closing almost half of them during the last 15 years. You can check here Stratexis comparison of Egyptian and European banking distribution.

Despite a large use of cash, finding money change is widely considered as a major pain point in Egypt -to the satisfaction of all workers depending on tips for their living- one of many symptoms that demonstrates the difficulty to manage cash in Egypt, particularly for banks.

Cash management is expensive, all economic agents will benefit from using it less

First, handling cash for a bank in an emerging market represents between 10%-15% of all logistical expenses. Several factors / sources contribute to amplify this type of expenses:

Cash collection and distribution from head office to branches

Cash collection and distribution from head office to the Central Bank

Cash counting in every stop (head office, cash transporters, branches)

Fraud

Deterioration of cash notes

Needless to mention, idle cash in circulation or deposited at branches and ATM represents a significant opportunity cost for banks.

In addition, we should consider the cost reduction opportunity of reallocating the workload of the following functions to commercial or analytical tasks:

Operational teams in branches (head of operations, tellers, dedicated staff for counting bills)

Internal controllers and security related staff

So, banks would be the first to benefit from the reduction of Cash use.

Enterprises and government will also benefit from the increase of electronic payments

Cash use is also generating large operational costs for major billers, which prefer to offer large incentives to the public to favor electronic payments:

Ride hailing companies offer free rides for card payers

Telecom operators offer discounts for automatic card payments

Fast food chains offer small gifts

The government is also interested by reducing the amount of cash operations for several reasons:

Reduce the informal economy

Accelerate financial inclusion and literacy, a strategic objective for the government

Improve anti-money laundering policies

Reduce the cost of printing cash notes

Optimize the government’s own running expenses

Let’s not forget about the Government Fiscal Management Information System (GFMIS) project, which aims to save up to 10% of operational expenditures.

The benefits for individuals are so obvious that they don’t need to be mentioned.

To conclude it seems that all economic actors have a major interest to reduce their use of cash, which will generate direct extra profits for banks and for the overall economy.

You will find here what a cashless society looks like

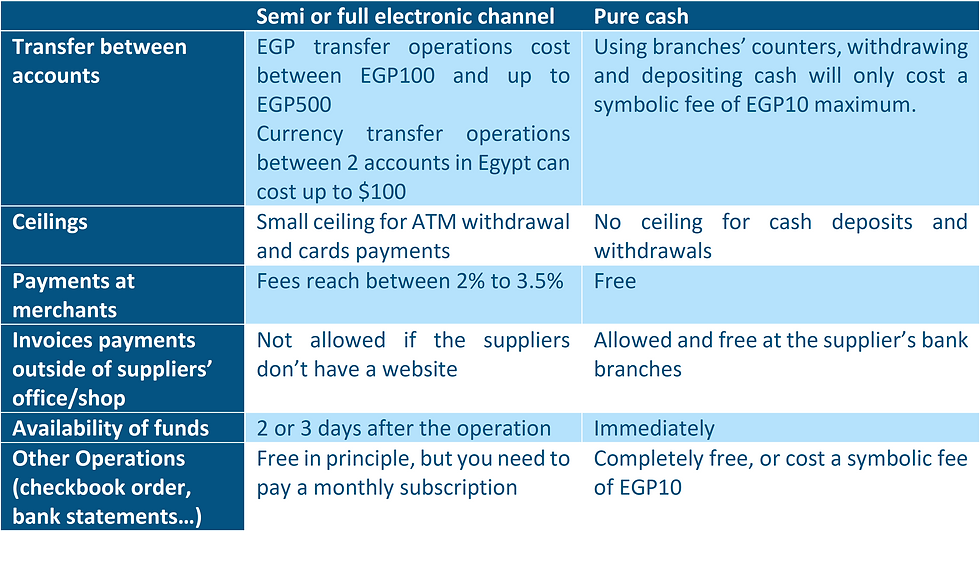

However, Cash remains favored by Egyptian banks

Regrettably, banks didn’t adapt their pricing yet to introduce a positive discrimination in favor of digital and electronic payments. Here are few examples of banking services whose prices and applications favor cash:

Electronic bank transfers are far more expensive and slower than manual cash withdrawals and deposits; currency transfers are even far more expensive even if both banks are in Egypt. At the opposite, cash withdrawals and deposits at the counter are either free or cost EGP10 only

Merchants endure high fees for electronic Payments (between 2% and 3.5%) of total amount, while cash payments are free

Clients can pay invoices at their suppliers’ bank only by cash, electronic payments are not allowed

Even worse, some of the recent measures discourage the use of ATM and banking cards in general:

Lower ceiling for ATM cash withdrawals to just EGP3000

Higher fees for withdrawing cash from competing banks’ ATM

Thus, if we compare some basic banking operations in terms of cost and availability, we will discover that banks are encouraging customers to use more cash in physical branches:

"Cash is king because it is reliable and available everywhere & anytime"

On top of these pricing benefits, Cash still holds additional advantages against electronic means of payment, that cannot be beaten any time soon: Cash is extremely reliable and is available wherever and whenever customers want; you can pay for everything in cash without any technical issues that forbid the operational execution. When it comes to educating inexperienced users, reliability and availability are powerful arguments to keep cash usage high and reject new means of payments.

The only actual cost for clients using cash that cannot be factored in this analysis is the time spent to conduct manual deposits and withdrawal operations. Some banks also introduced restrictions for cash operations under EGP5000. Remarkably, high net worth customers have an effective method to optimize this kind of costs; they use their personal/aides to replace them.

The consequence of the dominance of cash is that electronic payments are widely unused. Only an estimated 10% of the 30 million debit and credit cards are active in Egypt (at least an operation per month), out of which only 10% are used to make an actual payment transaction, the rest being a mean to withdraw cash from ATM only.

Fawry is bridging the gap between cash and electronic payments

When discussing Egyptian electronic payments, we should mention the tremendous success story of the fintech company “Fawry”. The success of Fawry comes from leveraging the best of the 2 means of payment: cash for its reliability and availability, and electronic systems for their seamless and fast processing. In a way, Fawry is educating unbanked population to trust electronic payments. Fawry would not have existed in a mature economy, where electronic payments are dominant. In that sense, Fawry is filling a gap left by banking players in Egypt. On its website, Fawry announces 65,000 payment locations in 300 Egyptian cities. As of December 2017, the central bank of Egypt declares 66,608 points of sale for the banking industry, which makes the reach of Fawry services equivalent to the reach of the whole banking industry. What is very promising is that the success of Fawry inspired a lot of other players to create fintech companies and contributed to the transformation of Egyptian financial services, which will bring higher value to Egyptian customers.

Here are some other Middle Eastern Fintech companies

So, what could banks do to seriously reduce cash use? A lot actually can be done

The current focus of banks and financial institutions is to create mobile wallets products. It's very difficult to differentiate the features of all these new products and customers' experience remains poor as the reliability and accessibility of these products are still considered low. Mobile wallets provided by telecom operators remain more competitive. At Stratexis, we already gave our point of view on how banks can learn from telecom operators to improve their operations.

Stratexis developed a complete framework for the digital transformation of payments. First, banking pricing should be rebalanced in favor of electronic channels:

Reduce payments commissions for merchants (0.2% to 0.5% is an appropriate level) increasing volumes will easily cover all operational expenses

Internet and mobile banking should be free, or at least included in payment cards fees

Develop/subsidize Points of Sale (POS) machines to enlarge their reach

Put barriers to cash deposits and withdrawals such as requiring a 48H notice when a client wants to withdraw an amount above a threshold

Make funds available overnight for electronic operations

Increase attractiveness of electronic transfers: they should be free when done via internet or mobile banking and cost cheaper fees when conducted by a teller

Banks can conduct this transformation by themselves, but most probably it will require regulatory reforms instructed by the Central Bank of Egypt or the National Council for Payments (NCP) created early 2017

As we mentioned earlier, one of the largest obstacles to develop electronic payments is operations’ reliability, which is often related to IT systems readiness. Which means that banks need to make large investments in their IT systems to significantly improve the quality and reliability of electronic operations.

The complexity of the IT systems that handles electronic operations prevents decision-makers from discussing technical issues and making the right decisions to encourage electronic operations expansion.

In addition to changing the pricing and to making operations more reliable, there are several actions that banks could undertake to reduce the cost of cash management. Stratexis has already been assisting its banking clients to include these initiatives in their own internal processes:

Review contracts with cash suppliers

Optimize cash circulation routes and number of stops at branches

Monitor cash levels in all branches and ATM to optimize idle cash

Develop dashboards to supervise cash operations Vs electronic operations

Streamline/outsource cash processes (collection, distribution, counting, payments…)

Set a global objective for electronic operations to reach a predefined % of the total number of operations and update the performance management system for branch managers and tellers

Introduce sanctions systems if discrepancies are regularly observed for some tellers

The National Council for Payments (NCP) needs to accelerate the adoption of reforms and transform Egypt into a cashless economy

The National Council for Payments (NCP) was created with a primary objective to transform Egypt into a cashless economy. President Sissi chaired the first 2 meetings in June and October 2017, alongside several key decision-makers of the banking industry, which demonstrates the importance and the priority given to this new public authority. The NCP represents the opportunity to coordinate all initiatives aiming to reduce the use of cash in the Egyptian economy. The main task in the short & medium term is to issue a law to accompany the development of non-cash financial transactions and that will include several proposals such as free mobile accounts opening and electronic means of payment in all government agencies.

What measures can the CBE implement?

As regulator, the Central Bank of Egypt (CBE) carries the huge responsibility to conduct painful reforms to change the habits of the Egyptian population. There are several proposals that could be conducted over the medium term:

Forbid the use of small cash change, while allowing small fractions in electronic transactions only. In that case, the inflation’s impact needs to be considered

Put limits on cash deposits and withdrawals in terms of amounts and availability

Set a ceiling for cash payments, which will make for instance the purchase of an apartment using only cash impossible; this ceiling should be gradually reduced to reach the European standards currently set at EUR 1000

Redefine identity controls obligations to favor electronic transactions at branches (for example allow card payments in branches for non-clients)

Set key performance indicators for banks, for example 80% of all operations to be conducted through electronic channels

In addition, several fines need to be implemented in the Egyptian financial law to sanction the following situations:

businesses refusing to install POS or electronic payments terminals

businesses refusing to be paid electronically

businesses applying higher tariffs for electronic payments

Of course, several international experiences are interesting to study to select what are the ones most adapted to the Egyptian market.

Lessons learned from the Indian reforms

If we want to discuss reducing cash in the economy and electronic payments, we must mention the results of the Indian government monetary decisions in November 2016. The prime minister Narendra Modi announced that the 500 and 1000-rupee bank notes representing 86.4% of total volume of rupee bills- cannot be used anymore and are to be withdrawn from the economy. A year and half later, the outcomes are considered positive, but not without an excessive cost for the economy; economic growth decelerated immediately after these measures and some sectors faced difficult business impacts.

Nevertheless, the major achievement of the Indian reforms was to strongly encourage the development of electronic payments and a cashless economy. forcing the Indian population to adapt quickly and learn how to use electronic payments. Annual growth for electronic payments scaled from being in the range of 20% to 50%, up to a new range of 40% to 70%. Modern tools such as Unique Payment Interface (UPI) along with other initiatives enabled Indian citizens to use their fingerprints for payments authentication; Indians can now pay as easily as they use their smartphones to call friends, without requiring a plastic card or a signature anymore. It’s a huge step towards reaching the cashless economy. Numerous other actions have accompanied the reforms but deserve longer study to be all presented and explained.

This new policy was mostly successful in reaching the financial inclusion of illiterate population but had unfortunately almost no impact on money laundering. 99% of the banknotes in circulation were laundered and sent back to the Central Bank, which means that informal operations are deeply rooted in the Indian economy and cannot be contained in a defined time-frame.

Egyptian officials certainly watched closely the results of the Indian experience. There are a lot of demonstrated benefits and lessons learned. One important lesson is that an ecosystem needs to be established before provoking such a shakedown and make electronic payments the only alternative. One of the prerequisites of such important reforms is the existence of efficient and reliable technological tools adapted to the illiterate population.

Is mobile wallets the answer ?

In the last 12 months, the number of digital wallets in the Egyptian market surged intensely. All banks seem eager to have their own wallet products. Knowing that the target users are mostly unbanked and have low incomes, one would wonder why banks invest so heavily to acquire customers who have little chance to be converted into profitable banking clients. The answer is mobile wallets could be the next big thing in terms of digital payments. Favored by softer registration conditions than traditional bank accounts, mobile wallet use has been growing very fast in the last few years. Vodafone cash, the comfortable leader of this market, already claims more than 4 Mn users, 33% more than the 3 Mn active bank accounts.

The growth in this business line is such that the future outcome cannot be predicted for the moment. Either mobile wallets will become the standard when it comes to digital payments or just a transition for more sophisticated digital means of payment. Until they reach a tipping point, the regulatory framework needs to be completed to avoid any loopholes that may hinder adoption.

In conclusion, the road to an Egyptian cashless economy is hard and requires a long-term plan shared by several players to eliminate all the cultural, regulatory and technological obstacles. Still, the ongoing reforms and observed growth in electronic payments is more than promising. According to PAYFORT Online Payment Gateway, electronic payments market in Egypt should reach $14.04bn by 2020. It appears to be a fantastic opportunity for the growing Egyptian Fintech ecosystem.

Author

Nadim Samna

Managing Partner

This post offers a fascinating comparison of how cultural, regulatory, and technological factors shape financial behavior across regions. As Egypt continues to rely heavily on cash while Europe embraces digital payments, the need for adaptable financial tools becomes increasingly clear. At FuncWallet, we provide exchange-ready crypto wallets that support seamless transitions between crypto and fiat—empowering users in both cash-heavy and cash-light economies to manage their assets securely and efficiently. Whether you're carrying cash or crypto, the right crypto Withdrawal wallet bridges the gap between tradition and transformation.